Adjusted trial balance example and explanation

But outside of the accountingdepartment, why is the adjusted trial balance important to the restof the organization? An employee or customer may not immediatelysee the impact of the adjusted trial balance on his or herinvolvement with the company. A company’s transactions are recorded in a general ledger and later summed to be included in a trial balance. Ending retained earnings information is taken from the statement of retained earnings, and asset, liability, and common stock information is taken from the adjusted trial balance as follows.

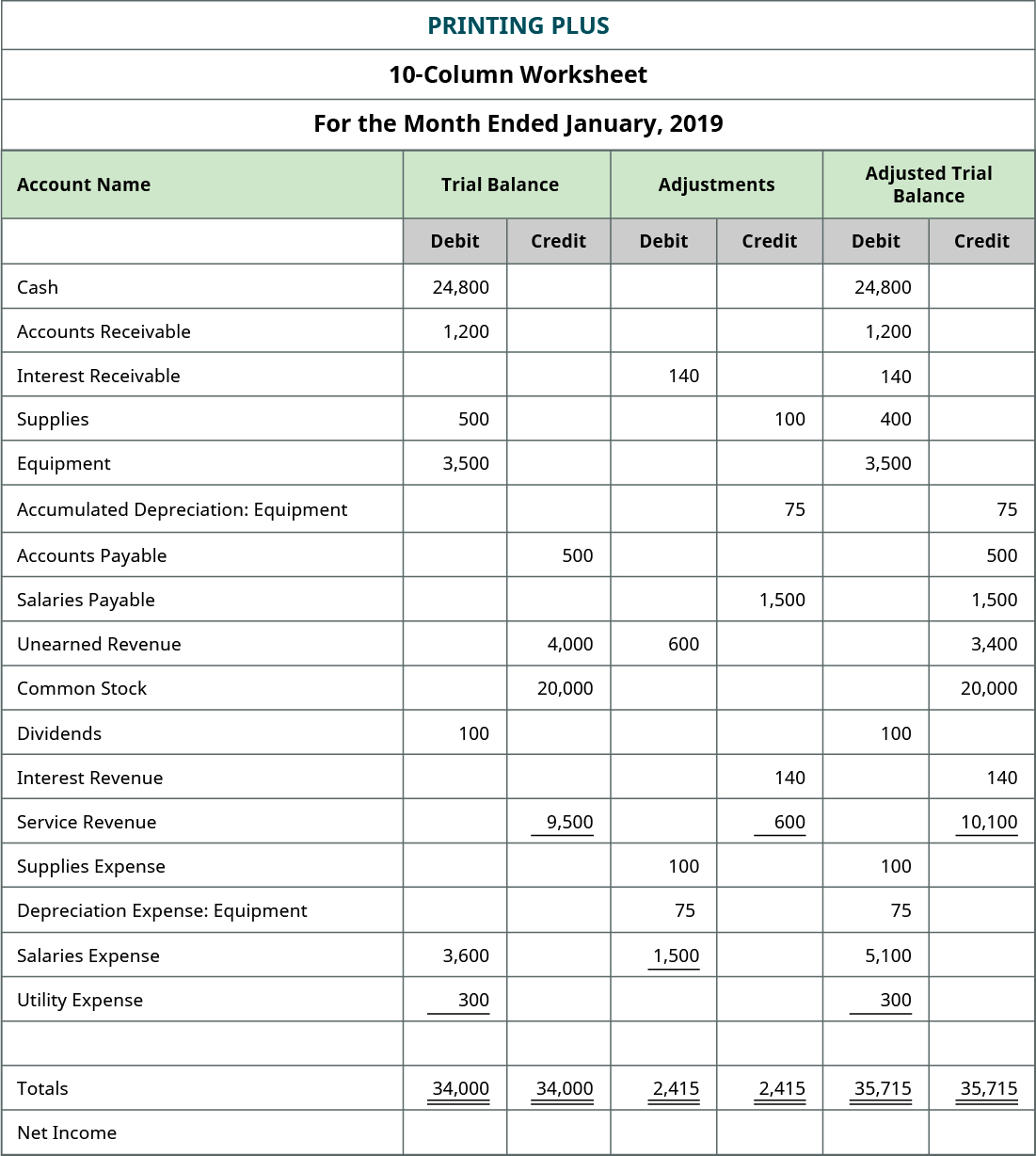

Ten-Column Worksheets

Liquidity refers to how easily an item can be converted to cash. IFRS requires that accounts be classified into current and noncurrent categories for both assets and liabilities, but no specific presentation format is required. Thus, for US companies, the first category always seen on a Balance Sheet is Current Assets, and the first account balance reported is cash. The accounts of a Balance Sheet using IFRS might appear as shown here. For example, IFRS-based financial statements are only required to report the current period of information and the information for the prior period. US GAAP has no requirement for reporting prior periods, but the SEC requires that companies present one prior period for the Balance Sheet and three prior periods for the Income Statement.

Trial Balance: Definition, How It Works, Purpose, and Requirements

- A trial balance simply shows a list of the ledger accounts and their balances.

- Both the debit and credit columns are calculated at the bottom of a trial balance.

- It acts as an auditing tool, while a balance sheet is a formal financial statement.

- Since most companies have computerized accounting systems, they rarely manually create a TB or have to check for out-of-balance errors.

- There are five sets of columns, each set having a column for debit and credit, for a total of 10 columns.

You will not see a similarity between the 10-column worksheetand the balance sheet, because the 10-column worksheet iscategorizing all accounts by the type of balance they have, debitor credit. To get the numbers in these columns, you take the number in thetrial balance column and add or subtract any number found in theadjustment column. There is no adjustment in the adjustment columns, so theCash balance from the unadjusted balance the better way to record prepayment amortisation in xero column is transferred overto the adjusted trial balance columns at $24,800. InterestReceivable did not exist in the trial balance information, so thebalance in the adjustment column of $140 is transferred over to theadjusted trial balance column. Presentation differences are most noticeable between the twoforms of GAAP in the Balance Sheet. Under US GAAP there is nospecific requirement on how accounts should be presented.

Adjusted Trial Balance Example

To simplify the procedure, we shall use the second method in our example. You could also take the unadjusted trial balance and simply add the adjustments to the accounts that have been changed. In many ways this is faster for smaller companies because very few accounts will need to be altered.

The list and the balances of the company’s accounts are presented after the adjusting journal entries are made at the year-end. Those balances are then reported on respective financial statements. Adjusted trial balance is not a part of financial statements; rather, it is a statement or source document for internal use. It is mostly helpful in situations where financial statements are manually prepared. If the organization is using some kind of accounting software, the bookkeeper or accountant just needs to pass the journal entries (including adjusting entries). The software automatically adjusts and updates the relevant ledger accounts and generates financial statements for the use of various stakeholders.

Adjusted Trial Balance

It shows a list of all accounts and their balances, either under the debit column or credit column. Both US-based companies and those headquartered in othercountries produce the same primary financial statements—IncomeStatement, Balance Sheet, and Statement of Cash Flows. One of the most well-known financial schemes is that involving the companies Enron Corporation and Arthur Andersen.

A trial balance only contains ending balances of your accounting accounts, while the general ledger has detailed transactions of the accounts. Notice the middle column lists the balance of the accounts with a debit balance, while the right column has balances for credits. Note that while a trial balance is helpful in the double-entry system as an initial check of account balances, it won’t catch every accounting error. The trial balance is a mathematical proof test to make sure that debits and credits are equal. Trial balances come in three key types, with each serving a purpose to help create accurate financial statements.

Once all ledger accounts and their balances are recorded, the debit and credit columns on the adjusted trial balance are totaled to see if the figures in each column match. Once all of the adjusting entries have been posted to the general ledger, we are ready to start working on preparing the adjusted trial balance. Preparing an adjusted trial balance is the sixth step in the accounting cycle. An adjusted trial balance is a list of all accounts in the general ledger, including adjusting entries, which have nonzero balances. This trial balance is an important step in the accounting process because it helps identify any computational errors throughout the first five steps in the cycle.

Let’s now take a look at the T-accounts and unadjusted trial balance for Printing Plus to see how the information is transferred from the T-accounts to the unadjusted trial balance. Debits and credits of a trial balance must tally to ensure that there are no mathematical errors. However, there still could be mistakes or errors in the accounting systems. A trial balance can be used to assess the financial position of a company between full annual audits. Take a couple of minutes and fill in the income statement and balance sheet columns. An income statement shows the organization’s financial performance for a given period of time.

Categories

- ! Без рубрики

- 0,003232118855

- 0,01495472361

- 0,0328410453

- 0,06443965059

- 0,06897055848

- 0,07229299461

- 0,08196605271

- 0,09993146312

- 0,1150445446

- 0,1274254951

- 0,1402535022

- 0,1728229818

- 0,1878789963

- 0,1881955746

- 0,1940455766

- 0,2255485814

- 0,2394029759

- 0,2458284738

- 0,2541064837

- 0,2839714422

- 0,293640919

- 0,3184669307

- 0,3222743898

- 0,3422332539

- 0,3485416783

- 0,3492169608

- 0,3681703285

- 0,376118532

- 0,3765272516

- 0,3880348002

- 0,3899898119

- 0,4210202669

- 0,4621212493

- 0,4820913545

- 0,5398581791

- 0,5411347575

- 0,580448841

- 0,5933233619

- 0,5979577874

- 0,6235427112

- 0,6288072013

- 0,6576286483

- 0,6729050496

- 0,6813945332

- 0,6869109112

- 0,7044794874

- 0,7048314585

- 0,7232184983

- 0,7322848938

- 0,7848181919

- 0,7870634885

- 0,8483834628

- 0,8492609359

- 0,8705737581

- 0,8772594557

- 0,8832594723

- 0,8910496418

- 0,8984255183

- 0,9054313909

- 0,9140200059

- 0,9370057378

- 0,9494435714

- 0,9557754463

- 0,9644652404

- 0,9655018094

- 0,9877876332

- 1

- 10000sat7

- 10050_tr

- 10060sat

- 10120_tr

- 10125_sat

- 10200_prod2

- 10200_sat

- 10200_tr

- 10310_sat

- 10350_tr

- 10350tr

- 10390_sat

- 10400_sat

- 10500_sat

- 10500_sat2

- 10500_wa2

- 10500_wa4

- 10520_tr

- 10550_tr

- 10700_sat

- 10700_wa

- 10800_prod

- 10900_wa

- 10cric-in.com

- 11000prod2

- 11000prod3

- 11200_prod

- 11400_wa

- 11700_wa

- 1xbet-games.onlin

- 2

- 21

- 26

- 3

- 30

- 31

- 32

- 6

- 7777777

- 8600_tr

- 8700_wa

- 9050_tr

- 9150tr

- 9500_wa2

- 9600_prod2

- 9600_sat

- 9600_sat2

- 9760_sat

- 9800_sat2

- 9870_sat

- 9890_wa

- 9900_sat2

- 9915_wa

- 9925_sat

- 9950_prod

- a legitimate mail order bride

- a mail order bride

- är postorder brud verklig

- Acheter la mariГ©e par correspondance

- acheter une mariГ©e par correspondance

- adobe generative ai 3

- Agence de messagerie de commande de mariГ©e

- Agence de vente par correspondance

- Agence de vente par correspondance avec la meilleure rГ©putation

- agences de mariГ©e par correspondance

- agencia de correo de orden de novia

- agencia de novias por correo

- agenzia di posta per ordini di sposa

- agenzia sposa per corrispondenza con la migliore reputazione

- AI in Cybersecurity

- aprBH

- aprBT

- aprBY

- aprCH

- AprGoF

- aprIPL

- aprMB

- aprPB

- aprProd

- aprRB

- aprSB

- Articles de la mariГ©e par correspondance

- Auf der Suche nach Ehe

- Auf der Suche nach einer Mail -Bestellung Braut

- Auslandische Brute

- average age of mail order bride

- average cost of a mail order bride

- average cost of mail order bride

- average mail order bride prices

- average price for a mail order bride

- average price for mail order bride

- average price of a mail order bride

- average price of mail order bride

- Aviator

- Avis des mariГ©es par correspondance

- bästa land för postorderbrud

- bästa legitima postorder brudens webbplatser

- bästa plats för postorderbrud

- bästa postorder brud webbplatser

- bästa postorder brudens webbplats

- bästa postorder brudens webbplatser reddit

- bästa postorderbrud någonsin

- bästa stället att få postorder brud

- BEST bewertete Versandauftragsbrautseiten

- best countries for a mail order bride

- best countries to get a mail order bride

- best country for mail order bride

- best country for mail order bride reddit

- best country to find a mail order bride

- best country to find mail order bride

- best legit mail order bride websites

- best mail order bride

- best mail order bride agency

- best mail order bride agency reddit

- best mail order bride companies

- best mail order bride company

- best mail order bride countries

- best mail order bride country

- best mail order bride ever

- best mail order bride places

- best mail order bride service

- best mail order bride site

- best mail order bride site reddit

- best mail order bride sites

- best mail order bride sites reviews

- best mail order bride website

- best mail order bride websites 2022

- best mail order bride websites reddit

- best place for mail order bride

- best place to get mail order bride

- best places for mail order bride

- best places to find mail order bride

- best places to get mail order bride

- best rangerte postordrebrudesider

- best rated mail order bride sites

- best real mail order bride site

- best real mail order bride sites

- best reputation mail order bride

- best site mail order bride

- best website to find a mail order bride

- best-tr-casinos

- Beste echte Mail -Bestellung Brautseite

- Beste echte Mail -Bestellung Brautseiten

- beste ekte postordre brudeside

- beste landet ГҐ finne en postordrebrud

- beste legit postordre brud nettsteder

- Beste legitime Mail -Bestellung Brautwebsites

- Beste Mail -Bestellung Braut

- Beste Mail -Bestellung Braut -Websites Bewertungen

- Beste Mail -Bestellung Braut Site Reddit

- Beste Mail -Bestellung Braut Websites 2022

- Beste Mail -Bestellung Brautagentur Reddit

- Beste Mail -Bestellung Brautfirma

- Beste Mail -Bestellung Brautpletze

- Beste Mail -Bestellung Brautseite

- Beste Mail -Bestellung Brautseiten

- Beste Mail -Bestellung Brautunternehmen

- Beste Mail -Bestellung Brautwebsite

- Beste Mail -Bestellung Brautwebsites

- Beste Mail bestellen Braut Websites Reddit

- beste nettsted post ordre brud

- Beste Orte, um Versandbestellbraut zu erhalten

- Beste Orte, um Versandbestellbraut zu finden

- beste postordre brud nettsted

- beste postordre brud nettsteder

- beste postordre brud nettsteder 2022

- beste postordre brud nettsteder reddit

- beste postordre brud nettstedet reddit

- beste postordre brud noensinne

- beste postordre brudbyrГҐ

- beste postordre brudebyrГҐ reddit

- beste postordre brudeside

- beste postordre brudland

- beste postordre brudselskaper

- beste postordrebrud

- Beste Reputation Mail -Bestellung Braut

- Beste Site -Mail -Bestellung Braut

- beste steder for postordrebrud

- beste steder ГҐ fГҐ postordrebrud

- Beste Versandbestellung Braut Land

- Beste Website, um eine Mail -Bestellung zu finden, Braut

- Bester Ort fГјr Versandbestellbraut

- Bester Ort, um Versandbestellbraut zu erhalten

- Bestes Land fГјr Versandbestellbraut

- Bestes Land fГјr Versandbestellbraut Reddit

- Bestes Land, um eine Versandbestellbraut zu finden

- Bestes Land, um Versandbestellbraut zu finden

- betandreas-azerbaijani.com

- betandreas-casinobd.com

- betandreas-yukle.com

- betify

- betwinner-maroc.com

- betwinner-sg.com

- betwinnermali.com

- BH

- bhnov

- bhtopjan

- Bir gelin sipariЕџ edebilir misin

- Bir posta siparişi gelini için en iyi ülkeler

- bir posta sipariЕџi gelini nasД±l evlenir

- Bir posta sipariЕџi gelini nerede bulabilirim

- Bitcoin

- bla gjennom postordrebruden

- blog

- bon site Web de mariГ©e par correspondance

- Bookkeeping

- Bookstime

- bra postorder brud webbplatser

- bra postorder brudens webbplats

- Braut bestellen Mail

- Braut Weltversandbraut Braute

- Breaking News

- Breaking-News

- BreakingNews

- bride mail order

- BRIDE MAILLEMENT BRIDE Bonne idГ©e?

- bride order mail

- bride order mail agency

- bride world mail order brides

- Bride World Order Mail Brides

- browse mail order bride

- brudbeställning postbyrå

- brudens världs postorder brudar

- brudeparets ordre bruder

- brudepostordre

- btbtnov

- bttopjan

- buenos sitios de novias por correo

- buon sito web per la sposa per corrispondenza

- buona posta elettronica siti sposa

- buscando una novia por correo

- buy a mail order bride

- buy essay online for cheap

- buy mail order bride

- buying a mail order bride

- can i get a mail order bride if i am already married?

- can you mail order a bride

- casino

- casino_online

- casino-news

- casino-online

- casinoluckystar.net

- casinos-nongamstop.uk19

- casinoways-games.com

- cataloghi di sposi per corrispondenza

- catalogo sposa per corrispondenza

- Catalogue de la mariГ©e par correspondance

- Catalogues de la commande par correspondance

- catГЎlogo de novias por correo

- cheap custom essay

- cheap custom essay services

- cheap custom essay writing

- cheap essay help online

- cheap essay writer

- cheap essay writing 24

- cheap write essay

- cheapest write my essay service

- chjan

- come funziona la sposa per corrispondenza

- come funziona una sposa per corrispondenza

- come funzionano i siti di sposa per corrispondenza

- come ordinare una sposa per corrispondenza

- come preparare un ordine postale sposa reddit

- come spedire una sposa

- come uscire con una sposa per corrispondenza

- Commandage mariГ©e Craigslist

- Commande de courrier Г©lectronique

- Commande par correspondance Definitiom

- Commande par courrier de la mariГ©e

- Commande par courrier lГ©gitime?

- commander par courrier une mariГ©e

- Commandez de la courrier mariГ©e rГ©elles histoires

- Commandez la mariГ©e rГ©el du site rГ©el

- Commandez par la poste pour de vrai?

- commanditГ©

- Comment acheter une mariГ©e par correspondance

- Comment commander de la mariГ©e

- Comment commander la commande par courrier mariГ©e

- Comment commander par la poste une mariГ©e

- Comment commander une mariГ©e par correspondance

- Comment commander une mariГ©e par correspondance russe

- Comment commander une mariГ©e russe mail

- Comment faire de la vente par la poste

- Comment faire une mariГ©e par correspondance

- Comment fonctionne la mariГ©e par courrier

- Comment fonctionnent la mariГ©e par courrier

- Comment fonctionnent les sites de mariГ©e par courrier

- Comment prГ©parer une mariГ©e par correspondance

- Comment prГ©parer une mariГ©e par correspondance Reddit

- Comment sortir avec une mariГ©e par correspondance

- Comment Г©pouser une mariГ©e par correspondance

- Commout Mail Entre Russian Bride

- compra la sposa per corrispondenza

- comprar una novia por correo

- comprare una sposa per corrispondenza

- correo de la novia orden

- correo en orden cuestan novia

- correo en orden definiciГіn de novia

- correo en orden novia

- correo legГtimo orden novia rusa

- correo orden cupГіn de novia

- correo orden de cuentos de novias reddit

- correo orden de cuentos reales de novias

- correo orden de reseГ±as del sitio web de la novia

- correo orden informaciГіn de la novia

- correo orden novia definitiom

- correo orden novia legГtima

- correo orden novia reveiw

- correo orden novia sitio real

- correo orden novia wiki

- correo orden sitios de novias reddit

- correo superior bride order web

- cos'ГЁ la sposa per corrispondenza

- cos'ГЁ la sposa per corrispondenza?

- cos'ГЁ una sposa per corrispondenza

- costo promedio de la novia del pedido por correo

- Coupon de mariГ©e par correspondance

- courrier des commandes de la mariГ©e

- Courrier pour commander la mariГ©e

- courrier Г©lectronique

- CoГ»t moyen de la mariГ©e par correspondance

- Creative

- Cryptocurrency exchange

- custom essay writers really cheap

- custom essay writing service cheap

- cГіmo casarse con una novia por correo

- cГіmo enviar por correo a la novia

- cГіmo pedir una novia rusa por correo

- cГіmo preparar un correo orden novia reddit

- cГіmo salir con una novia por correo

- Datation de la mariГ©e par correspondance

- dati sposa per corrispondenza

- deberГa salir con una novia por correo

- decch

- Definicija usluga za mladenke

- definisjon av postordre brud tjenester

- definizione dei servizi per la sposa per corrispondenza

- definizione sposa per corrispondenza

- devrais-je acheter une mariГ©e par correspondance

- devrais-je sortir avec une mariГ©e par correspondance

- diabetes

- Die Mail -Bestellungsbrautstelle

- Die Versandbestellbraut

- diez mejores sitios web de novias por correo

- donde compro una orden de correo novia

- dove acquistare una sposa per corrispondenza

- dove trovare una sposa per corrispondenza

- dovrei comprare una sposa per corrispondenza

- Durchschnittliche Kosten einer Versandbestellbraut

- Durchschnittliche Kosten fГјr Versandbestellbraut

- Durchschnittliche Versandauftragspreise

- Durchschnittsalter der Postanweisung Braut

- Durchschnittspreis fГјr eine Versandbestellbraut

- DГ©couvrez la mariГ©e par correspondance

- DГ©finition de la mariГ©e par correspondance

- DГ©finition des services de vente par correspondance

- dГіnde comprar una novia por correo

- e-mail order bride

- E-Mail-Bestellung Braut

- e-post ordre brud nettsted anmeldelser

- E-posta SipariЕџi Gelin

- e-postordre brud nettsteder anmeldelser

- Echte Versandbestellbraut -Sites

- Echte Versandbestellbrautwebsites

- Echte Versandungsbraut

- Echter Mail -Bestellung Brautservice

- ed

- Eine Versandauftragsbraut

- ekte postordre brud nettsted

- ekte postordre brudhistorier

- ekte postordrebrud

- En iyi 10 posta sipariЕџi gelini

- En iyi 5 posta sipariЕџi gelin sitesi

- En iyi posta sipariЕџi gelin Гјlkesi nedir

- En iyi posta sipariЕџi gelini sitesi

- En iyi posta sipariЕџi gelini web siteleri reddit

- En iyi site posta sipariЕџi gelin

- en legitim postorderbrud

- en legitim postordrebrud

- En Д°yi Posta SipariЕџi Gelin Siteleri Д°ncelemeleri

- En Д°yi Posta SipariЕџi Gelin Ећirketi

- En Д°yi Yasal Posta SipariЕџi Gelin Web Siteleri

- encontrar una novia

- encontrar una novia por correo

- encuГ©ntrame una novia por correo

- er postordre brud ekte

- er postordrebrud en ekte ting

- es la novia del pedido por correo algo real

- essay writers cheap

- etsitkö postimyynti morsiamaa

- etГ media della sposa per corrispondenza

- FairSpin

- Faits de mariГ©e par correspondance

- farmakeioorama.gr

- fastbet-live.com

- femme de commande par correspondance

- fi

- find a bride

- find a mail order bride

- find mail order bride

- find me a mail order bride

- Finden Sie eine Braut

- finding a mail order bride

- finn meg en postordrebrud

- finne en postordrebrud

- FinTech

- flashdash-nodepositbonus.com

- foreign brides

- Forex Trading

- fr

- freshbet

- gacor-slot

- game-casino

- gdje kupiti mladenku za narudЕѕbu poЕЎte

- gdje mogu kupiti mladenku za narudЕѕbu poЕЎte

- gdje mogu pronaći mladenku za narudžbu pošte

- gdje pronaći mladenku za narudžbu pošte

- Gelin DГјnya Posta SipariЕџi Gelinleri

- Gelin SipariЕџ Posta AjansД±

- Gelin SipariЕџ PostasД±

- Gelin siparişi vermek için posta

- General

- generative ai application landscape 1

- generative ai in healthcare

- genomsnittliga postorder brudpriser

- genomsnittspris för en postorderbrud

- Gerçek Posta Siparişi Gelin Web Sitesi

- Gerçek posta siparişi gelini sitesi

- gewichtsverlies

- gjennomsnittlig kostnad for postordrebruden

- gjennomsnittlige postordre brudpriser

- gjennomsnittsalder for postordrebruden

- gjennomsnittspris pГҐ en postordrebrud

- gjennomsnittspris pГҐ postordrebruden

- god postordre brud nettsted

- good mail order bride sites

- good mail order bride website

- gpt 5 capabilities 5

- Gute Mail -Bestellung Brautseiten

- Gute Mail -Bestellung Brautwebsite

- haluan postimyynti morsiamen

- heiГџeste Mail -Bestellung Braut

- hello world

- help me write my essay online

- histoire vraie de la mariГ©e par correspondance

- histoires de la mariГ©e par correspondance rГ©elle

- histoires de la mariГ©e par la courrier Г©lectronique

- Histoires de mariГ©e par correspondance reddit

- Histoires de vente par correspondance

- historia correo orden novia

- historia de la novia del pedido por correo

- historia om postorderbruden

- historia real de la novia del pedido por correo

- historiapostitilaus morsian

- historias de novias de pedidos por correo

- historie postordre brud

- historien til postordrebruden

- Historique de la mariГ©e par correspondance

- History -Mail -Bestellung Braut

- history mail order bride

- history of mail order bride

- hitta en postorderbrud

- hitta mig en postorderbrud

- Hot -Mail -Bestellung Braut

- hot mail order bride

- hot mail ordre brud

- hottest mail order bride

- how do mail order bride sites work

- how do mail order bride work

- how does a mail order bride work

- how does mail order bride work

- how does mail order bride works

- how to buy a mail order bride

- how to date a mail order bride

- how to do a mail order bride

- how to do mail order bride

- how to mail order a bride

- how to mail order bride

- how to marry a mail order bride

- how to order a mail order bride

- how to order a mail russian bride

- how to order a russian mail order bride

- how to order mail order bride

- how to prepare a mail order bride

- how to prepare a mail order bride reddit

- huipputarjous morsiamen maat

- hur fungerar en postorderbrud

- hur fungerar postorderbruden

- hur man beställer en rysk brud

- hur man förbereder en postorderbrud

- hur man gör postorder brud

- hur man går med en postorderbrud

- hur man skickar beställning brud

- hur man skickar en beställning av en brud

- hva en postordrebrud

- hva er den beste postordrebrudtjenesten

- hva er det beste postordre brudlandet

- Hva er en postordre brud

- hva er en postordrebrud

- hva er en postordrebrud?

- hva er postordre brud tjenester

- hva er postordrebrud

- hva er postordrebrud?

- hva er postordrebruden?

- hva er som postordrebrud

- hvor du kan kjГёpe en postordrebrud

- hvor finner jeg en postordrebrud

- hvor kan jeg finne en postordrebrud

- hvor kan jeg fГҐ en postordrebrud

- hvordan bestille en russisk postordrebrud

- hvordan du bestiller en postordrebrud

- hvordan du forbereder en postordrebrud

- hvordan du gjГёr en postordrebrud

- hvordan du gjГёr postordrebrud

- hvordan du kan sende en brud pГҐ mail

- hvordan fungerer en postordrebrud

- hvordan fungerer postordrebruden

- hvordan kjГёpe en postordrebrud

- i 10 migliori siti web di sposa per corrispondenza

- i 5 migliori siti di sposa per corrispondenza

- i migliori paesi della sposa per corrispondenza

- i migliori paesi per una sposa per corrispondenza

- i migliori posti per la sposa per corrispondenza

- i migliori siti di sposa per corrispondenza.

- i posti migliori per ricevere la sposa per corrispondenza

- i want a mail order bride

- in cerca di una sposa per corrispondenza

- Industrie des mariГ©es par correspondance

- Industrija mladenke

- Informacije o mladenki

- Informations sur les mariГ©es par correspondance

- Insights

- internasjonal postordrebrud

- international mail order bride

- Interracial Mail -Bestellung Braut

- interracial mail order bride

- interracial postordre brud

- is mail order bride a real thing

- is mail order bride real

- is mail order bride safe

- is mail order bride worth it

- Ist die Versandbraut real

- Ist Versandbestellbraut eine echte Sache

- Ist Versandbestellbraut sicher

- IT Education

- IT Vacancies

- IT Вакансії

- IT Образование

- izzi

- jardiance

- Je li mladenka narudЕѕba prava prava stvar

- Je veux une mariГ©e par correspondance

- jeg vil ha en postordrebrud

- köp postorder brud

- kaikkien aikojen paras postimyynti

- Kako izlaziti mladenka za narudЕѕbu poЕЎte

- Kako napraviti mladenku za narudЕѕbu poЕЎte

- Kako naruДЌiti mladenku za narudЕѕbu poЕЎte

- Kako naruДЌiti poЕЎtu ruske mladenke

- Kako pripremiti mladenku za narudЕѕbu poЕЎte

- Kako radi mladenka za narudЕѕbu poЕЎte

- Kako radi narudЕѕbe za narudЕѕbu poЕЎte

- Kako se vjenДЌati mladenka za narudЕѕbu poЕЎte

- Kakva narudЕѕba poЕЎte

- kan du sende en brud pГҐ mail

- Kann ich eine Versandungsbraut bekommen, wenn ich bereits verheiratet bin?

- kansainvälinen postimyynti morsian

- Kauf einer Mail -Bestellung Braut

- Kaufen Sie eine Mail -Bestellung Braut

- Koja je najbolja naredba za mladenku

- koja je narudЕѕba poЕЎte

- kuinka tehdä postimyynti morsiamen

- kuinka tilata morsiamen postitse

- kuinka tilata postimyynti morsiamen

- kuinka valmistaa postimyynti morsiamen

- kuuma postimyynti morsian

- kymmenen eniten postimyynti morsiamen sivusto

- kz-betandreas.com

- Können Sie eine Braut bestellen?

- La courrier Г©lectronique en vaut la peine?

- la mariГ©e par correspondance

- La mariГ©e par correspondance en vaut la peine

- La mariГ©e par correspondance est-elle rГ©elle

- La mariГ©e par correspondance est-elle sГ»re

- La mariГ©e par correspondance est-elle une chose rГ©elle

- la sposa per corrispondenza

- laillinen postimyynti morsian

- lailliset postimyynti morsiamen palvelut

- lailliset postimyynti morsiamen sivustot

- lailliset postimyynti morsiamen verkkosivustot

- laopcion.com.co

- latest-news

- Le site de la mariГ©e par correspondance

- legale Versandhandel Seiten für Bräute

- Leggit Mail bestellen Brautseiten

- leggit mail order bride sites

- leggit post beställning brud webbplatser

- leggit postordre brud nettsteder

- Legit Mail NarudЕѕba mladenka

- Legit Mail narudЕѕbe mladenke web stranice Reddit

- legit mail order bride

- legit mail order bride service

- legit mail order bride site

- legit mail order bride sites

- legit mail order bride sites reddit

- legit mail order russian bride

- legit postimyynti morsiamen palvelu

- legit postimyynti morsiamen sivustot

- legit postimyynti morsian

- legit postimyynti venäläinen morsian

- legit postordre brud

- legit postordre brud nettsted

- legit postordre brud nettsteder

- legit postordre brud nettsteder reddit

- legit postordre brudtjeneste

- legit postordre russisk brud

- legitim postorder brudens webbplatser

- legitim postorder brudtjänster

- legitim postordrebrud

- legitimale Mail -Bestellung Braut

- legitimale Versandbestellung russische Braut

- legitimate mail order bride

- legitimate mail order bride companies

- legitimate mail order bride services

- legitimate mail order bride site

- legitimate mail order bride sites

- legitimate mail order bride website

- legitimate mail order bride websites

- legitime Mail -Bestellung Braut Site

- legitime Mail -Bestellung Brautdienste

- legitime Mail bestellen Brautunternehmen

- Legitime Mail bestellen Brautwebsite

- legitime Mail bestellen Brautwebsites

- legitime postordrebrud nettsteder

- legitime postordrebrudesider

- legitime postordrebrudselskaper

- legitime Versandbestellbraut

- legitime Versandbestellbrautstandorte

- legitimer Versandauftragsbrautservice

- legitimert postordre brudtjeneste

- legitimna web stranica za mladenku

- legitimne tvrtke za mladenke

- legitimne web stranice za mladenke

- legitimt postordrebrud nettsted

- Legitimte -Mail -Bestellung Brautservice

- legitimte mail order bride service

- legititna poЕЎta naredba ruska mladenka

- legittimare il servizio di sposa per corrispondenza

- Les meilleurs pays pour obtenir une mariГ©e par correspondance

- Les meilleurs sites de mariГ©es par correspondance.

- Les sites de mariГ©e par correspondance lГ©gitimes

- lesbian mail order bride

- lesbian mail order bride reddit

- lesbisk postordre bruden reddit

- lesbisk postordrebrud

- lesbo postimyynti morsian

- Lezbijska narudЕѕba za mladenku Reddit

- list of best mail order bride sites

- lista över bästa postorderbrudsajter

- lista de los mejores sitios para novias por correo

- Liste der besten Mail -Bestell -Braut -Sites

- Liste des meilleurs sites de mariГ©es par correspondance

- liste over beste postordre brudsider

- looking for a mail order bride

- looking for marriage

- lovecasino-review.com

- luckstar.site

- lucky-jett.org

- luckystar-casino.net

- luckystar123club.org

- luckystaraviatorin.org

- luckystaraviatorindia.org

- luckystarlogin.in

- lyrica

- Mail -Bestellung Braut

- Mail -Bestellung Braut -Websites ?ГјberprГјfen

- Mail -Bestellung Braut Datierung

- Mail -Bestellung Braut definieren

- Mail -Bestellung Braut echt

- Mail -Bestellung Braut es wert ist

- Mail -Bestellung Braut legitim

- Mail -Bestellung Braut real

- Mail -Bestellung Brautagentur mit dem besten Ruf

- Mail -Bestellung Brautagenturen

- Mail -Bestellung Brautbewertung

- Mail -Bestellung Brautdefinition

- Mail -Bestellung Brautdienste

- Mail -Bestellung Brautdienste Definition

- Mail -Bestellung Brautindustrie

- Mail -Bestellung Brautkatalog

- Mail -Bestellung Brautkataloge

- Mail -Bestellung Brautkupon

- Mail -Bestellung Brautservice

- Mail -Bestellung Bride Agency Reviews

- Mail an die Braut bestellen

- Mail bestellen Braut -Website -Bewertungen

- Mail bestellen Braut Arbeit?

- Mail bestellen Braut Craigslist

- Mail bestellen Braut echte Geschichten

- Mail bestellen Braut FAQ

- Mail bestellen Braut gute Idee?

- Mail bestellen Braut legitim

- Mail bestellen Braut legitim?

- Mail bestellen Braut Reales Standort

- Mail bestellen Braut Reveiw

- Mail bestellen Braut Websites Bewertungen

- Mail bestellen Braut Websites Reddit

- Mail bestellen Braut Wikipedia

- Mail bestellen Brautartikel

- Mail bestellen Brautbewertungen

- Mail bestellen Brautgeschichten

- Mail bestellen Brautgeschichten Reddit

- Mail bestellen Brautinformationen

- Mail bestellen Brautlender

- Mail bestellen Brautseiten

- Mail bestellen Brautstandorte legitim

- Mail bestellen Brautwebes Reddit

- Mail bestellen Brautwebsite

- Mail bestellen Brautwebsites

- Mail bestellen eine Braut

- Mail bestellen Frauen

- mail bride order

- mail brudbeställning

- Mail dans l'ordre de la mariГ©e

- Mail dans l'ordre du coГ»t de la mariГ©e

- Mail dans la dГ©finition de la mariГ©e

- mail för att beställa brud

- mail for brudekostnad

- mail for ГҐ bestille brud

- mail i ordning bruddefinition

- mail i rekkefГёlge brud

- Mail in der Bestellung Brautdefinition

- mail in order bride

- mail in order bride cost

- mail in order bride definition

- mail in ordine definizione sposa

- Mail Mail

- Mail narudЕѕba Katalog mladenke

- Mail narudЕѕba mladenka definira

- Mail narudЕѕba mladenka stvarna

- Mail narudЕѕba mladenka vrijedi?

- Mail narudЕѕbe mladenke za stvarno

- Mail narudЕѕbe za mladenke legitimne

- Mail narudЕѕbe za mladenke ДЌinjenice

- mail on order bride

- mail order a bride

- mail order bride

- mail order bride agences

- mail order bride agencies

- mail order bride agency

- mail order bride agency reviews

- mail order bride agency with the best reputation

- mail order bride articles

- mail order bride catalog

- mail order bride catalogs

- mail order bride catalogue

- mail order bride countries

- mail order bride coupon

- mail order bride craigslist

- mail order bride dating

- mail order bride dating site

- mail order bride dating sites

- mail order bride define

- mail order bride definitiom

- mail order bride definition

- mail order bride facts

- mail order bride faq

- mail order bride for real

- mail order bride for real?

- mail order bride for sale

- mail order bride good idea?

- mail order bride industry

- mail order bride info

- mail order bride information

- mail order bride legit

- mail order bride legit sites

- mail order bride legit?

- mail order bride real

- mail order bride real site

- mail order bride real stories

- mail order bride reveiw

- mail order bride review

- mail order bride reviews

- mail order bride service

- mail order bride services

- mail order bride services definition

- mail order bride sites

- mail order bride sites legitimate

- mail order bride sites reddit

- mail order bride sites review

- mail order bride stories

- mail order bride stories reddit

- mail order bride story

- mail order bride website

- mail order bride website reviews

- mail order bride websites

- mail order bride websites reddit

- mail order bride websites reviews

- mail order bride wiki

- mail order bride wikipedia

- mail order bride work?

- mail order bride worth it

- mail order bride worth it?

- mail order sposa informazioni

- mail order wife

- mail order wives

- mail ordina una sposa

- mail på beställning brud

- mail to order bride

- mail-order bride

- Mail-Order-Braut

- mail-order-bride

- Mail. Bride Legit

- maila i ordning brud

- Mailbrautbestellung

- mariГ©e par correspondance

- mariГ©e par correspondance chaude

- mariГ©e par correspondance dГ©finir

- mariГ©e par correspondance en ligne

- mariГ©e par correspondance internationale

- mariГ©e par correspondance interraciale

- mariГ©e par correspondance la plus chaude

- mariГ©e par correspondance lesbienne

- mariГ©e par correspondance lГ©gitime

- mariГ©e par correspondance pour de vrai

- mariГ©e par correspondance reveiw

- mariГ©e par correspondance rГ©elle

- mariГ©e par correspondance wikipedia

- mariГ©e par correspondance Г vendre

- mariГ©e par la poste d'historique

- medic

- Meilleur endroit pour obtenir la mariГ©e par correspondance

- Meilleur endroit pour obtenir une mariГ©e par correspondance

- Meilleur pays de mariГ©e par correspondance

- Meilleur pays pour la mariГ©e par correspondance

- Meilleur pays pour la mariГ©e par correspondance Reddit

- Meilleur pays pour trouver la mariГ©e par correspondance

- Meilleur pays pour trouver une mariГ©e par correspondance

- Meilleur service de mariГ©e par correspondance

- Meilleur site de mariГ©e par correspondance

- Meilleur site de mariГ©e par correspondance rГ©el

- Meilleur site Web de mariГ©e par correspondance

- Meilleure agence de mariГ©e par correspondance

- Meilleure agence de mariГ©e par correspondance reddit

- Meilleure entreprise de mariГ©e par correspondance

- Meilleure mariГ©e par correspondance

- Meilleure mariГ©e par correspondance de tous les temps

- Meilleures sociГ©tГ©s de mariГ©es par correspondance

- Meilleurs avis sur les sites de mariГ©e par correspondance

- Meilleurs endroits pour la mariГ©e par correspondance

- meilleurs pays pour une mariГ©e par correspondance

- Meilleurs sites de mariГ©e par correspondance

- Meilleurs sites de mariГ©s par correspondance rГ©el

- Meilleurs sites Web de mariГ©e par correspondance lГ©gitime

- Meilleurs sites Web de mariГ©es par correspondance reddit

- mejor correo orden novia agencia reddit

- mejor lugar para recibir un pedido por correo novia

- mejor orden de correo novia

- mejor sitio web para encontrar una novia por correo

- mejores lugares para la novia por correo

- mejores lugares para recibir pedidos por correo novia

- mejores paГses de novias por correo

- MeЕџru bir posta sipariЕџi gelini

- MeЕџru posta sipariЕџi gelin web siteleri

- miglior ordine postale agenzia sposa reddit

- miglior ordine postale sposa paese

- miglior paese per la sposa per corrispondenza

- miglior paese per trovare una sposa per corrispondenza

- miglior servizio di sposa per corrispondenza

- miglior sito per corrispondenza sposa

- miglior sito per sposa per corrispondenza reale

- migliore agenzia sposa per corrispondenza

- migliore sposa per corrispondenza

- migliori compagnie di sposa per corrispondenza

- migliori paesi sposa per corrispondenza

- migliori siti di sposa per corrispondenza

- migliori siti web di sposa ordinazione per corrispondenza

- migliori vendita per corrispondenza siti web sposa 2022

- mikä on paras postimyynti morsiamen maa

- mikä on postimyynti morsian

- mikä on postimyynti morsian?

- MINDES MINDES Web lokacije.

- mistä löydän postimyynti morsiamen

- mistä ostaa postimyynti morsiamen

- mistä ostan postimyynti morsiamen

- miten postimyynti morsiamen sivustot toimivat

- miten postimyynti morsiamen toimii

- miten postimyynti morsian toimii

- Mjesto za mladenku s gornjom poЕЎtom

- mladenka s najviЕЎe poЕЎte

- mladenka za meД‘usobnu narudЕѕbu poЕЎte

- mladenka za narudЕѕbu poЕЎte

- mladenke na narudЕѕbi najbolje poЕЎte

- Mogu li dobiti mladenku za narudžbu pošte ako sam već oženjen?

- morsiamen postimyynti

- morsiamen tilausposti

- MoЕѕete li naruДЌiti mladenku

- n_bh

- n_bt

- n_pb

- Najbolja mjesta za dobivanje mladenke za narudЕѕbu poЕЎte

- Najbolja narudЕѕba Mail ikad

- Najbolja narudЕѕba za mladenke

- Najbolja narudЕѕba za mladenku

- Najbolja narudЕѕba za mladenku Reddit

- Najbolja reputacija narudЕѕbe mladenke

- Najbolja zemlja za mladenku za narudЕѕbu poЕЎte

- Najbolja zemlja za narudЕѕbu poЕЎte Reddit

- Najbolja zemlja za pronalaЕѕenje mladenke za narudЕѕbu poЕЎte

- Najbolje mjesto za dobivanje mladenke za narudЕѕbu poЕЎte

- Najbolje mjesto za mladenku za narudЕѕbu poЕЎte

- Najbolje narudЕѕbe za mladenke 2022

- Najbolje narudЕѕbe za mladenke recenzije

- Najbolje narudЕѕbe za mladenke web stranice

- Najbolje ocijenjene web stranice za mladenke

- Najbolje web stranice za mladenke prave poЕЎte

- najbolje zemlje za mladenku za narudЕѕbu poЕЎte

- narudЕѕba mail mladenke

- NarudЕѕba poЕЎte

- NarudЕѕba poЕЎte Legit?

- narudЕѕba poЕЎte mladenka craigslist

- narudЕѕba poЕЎte mladenka reveiw

- narudЕѕba poЕЎte mladenka wikipedia

- NaruДЌivanje poЕЎte FAQ FAQ

- NaruДЌivanje poЕЎte mladenke

- NaruДЌivanje poЕЎte supruge

- NaruДЌivanje za mladenku kupon

- nastya

- Ne posta sipariЕџi gelin

- Nevjesta narudЕѕba poЕЎte

- new

- New Post

- new-games

- News

- News top

- news-top

- NEWSTOP

- nl

- novia orden mundial de correo novias

- on postimyynti morsiamen turvallinen

- on postimyynti morsian todellinen

- online mail order bride

- online postordre brud

- online-postitilaus morsian

- orden de correo de la industria de la novia

- orden de correo de la novia

- orden de correo de las agencias de la novia

- orden de correo electrГіnico novia

- orden de correo en lГnea novia

- orden de correo internacional novia

- orden de correo legГtimo novia

- orden de correo novia

- orden de correo novia de verdad?

- orden de correo novia definir

- orden de correo novia vale la pena

- orden de correo novia vale la pena?

- ordenar por correo historias de novias

- ordine della posta della sposa

- ordine postale sposa definire

- ordine postale sposa definizione

- ordine postale sposa legittima?

- ordini postali agenzie sposa

- oГ№ acheter une mariГ©e par correspondance

- OГ№ puis-je acheter une mariГ©e par correspondance

- oГ№ puis-je trouver une mariГ©e par correspondance

- oГ№ trouver une mariГ©e par correspondance

- paras paikka postimyynti morsiamenelle

- paras paikka saada postimyynti morsiamen

- paras postimyynti morsiamen sivusto

- paras sivustopostitilaus morsian

- parhaat legit postimyynti morsiamen verkkosivustot

- parhaat maat postimyynti morsiamen kanssa

- parhaat paikat löytää postimyynti morsiamen

- parhaat paikat saada postimyynti morsiamen

- parhaat postimyynti morsiamen verkkosivustot reddit

- parhaiten arvioitu postimyynti morsiamen palvelu

- pay for essay paper

- pay for someone to write an essay

- Pays des mariГ©es par correspondance

- PB

- pb_dec

- pbnov

- pbtopjan

- pedido por correo novia en venta

- pedidos por correo de reseГ±as de agencias de novias

- pedidos por correo sitios de novias legГtimos

- per corrispondenza

- per corrispondenza craigslist sposa

- per corrispondenza i siti della sposa reddit

- per corrispondenza paesi sposa

- per corrispondenza sposa faq

- per corrispondenza sposa siti web reddit

- per corrispondenza sposa storia

- per corrispondenza storie di sposi

- Pinco türkiye

- Pinup

- Pinup casino

- pitäisikö minun päivätä postimyynti morsiamen

- pınco

- Podaci o narudЕѕbi poЕЎte

- posso ottenere una sposa per corrispondenza se sono giГ sposato?

- Post in der Bestellung Braut

- Post in der Bestellung Brautkosten

- Post_3_1

- Posta Gelin SipariЕџi

- posta in ordine sposa

- Posta NasД±l SipariЕџ Edilir Rus Gelin

- posta per ordinare la sposa

- posta sipariЕџi

- Posta SipariЕџi Gelin

- Posta SipariЕџi Gelin AjanslarД±

- Posta SipariЕџi Gelin Bilgisi

- Posta Siparişi Gelin Gerçek Site

- Posta Siparişi Gelin Gerçekleri

- posta sipariЕџi gelin hikayeleri reddit

- Posta SipariЕџi Gelin Hizmetleri Nedir

- Posta SipariЕџi Gelin NasД±l SatД±n AlД±nД±r

- Posta SipariЕџi Gelin NasД±l YapД±lД±r

- posta sipariЕџi gelin nasД±l Г§alД±ЕџД±r

- Posta SipariЕџi Gelin Nedir

- Posta SipariЕџi Gelin Web Siteleri

- Posta SipariЕџi Gelin Web Sitesi

- Posta SipariЕџi Gelin Д°ncelemesi

- Posta siparişi gelini almak için en iyi yer

- Posta siparişi gelini almak için en iyi yerler

- posta sipariЕџi gelini gГјvenli mi

- Posta sipariЕџi gelini istiyorum

- posta siparişi gelini için en iyi ülke

- Posta sipariЕџi gelini nedir

- Posta SipariЕџi Gelini SatД±n AlД±n

- Posta Siparişi Gelininin Gerçek Hikayesi

- Posta sipariЕџi karД±sД±

- postimyynti morsiamen agences

- postimyynti morsiamen arvoinen?

- postimyynti morsiamen historia

- postimyynti morsiamen keski-ikä

- postimyynti morsiamen keskimääräinen hinta

- postimyynti morsiamen keskimääräiset kustannukset

- postimyynti morsiamen luettelo

- postimyynti morsiamen myytävänä

- postimyynti morsiamen oikeita tarinoita

- postimyynti morsiamen palvelut

- postimyynti morsiamen sivustojen arvostelu

- postimyynti morsiamen sivustot

- postimyynti morsiamen sivustot lailliset

- postimyynti morsiamen sivustot reddit

- postimyynti morsiamen tarinoita reddit

- postimyynti morsiamen tiedot

- postimyynti morsiamen treffit

- postimyynti morsiamen työ?

- postimyynti morsiamen verkkosivusto

- postimyynti morsiamen verkkosivustojen arvostelut

- postimyynti morsian

- postimyynti morsian reveiw

- postimyynti morsian todellinen

- postimyynti vaimo

- postimyynti-morsian

- posto migliore per ricevere la sposa per corrispondenza

- postorder brud

- postorder brud agences

- postorder brud artiklar

- postorder brud legit?

- postorder brud på riktigt?

- postorder brud värt det

- postorder brud verklig webbplats

- postorder brudens webbplats

- postorder brudens webbplats recensioner

- postorder brudesidor reddit

- postorder brudhistoria

- postorder brudhistorier

- postorder brudhistorier reddit

- postorder brudinfo

- postorder brudkatalog

- postordre brud

- postordre brud agences

- postordre brud craigslist

- postordre brud datingside

- postordre brud definere

- postordre brud definisjon

- postordre brud ekte nettsted

- postordre brud for ekte

- postordre brud god idГ©?

- postordre brud historier reddit

- postordre brud legit

- postordre brud legit nettsteder

- postordre brud legit?

- postordre brud nettsteder

- postordre brud nettsteder gjennomgang

- postordre brud nettsteder legitime

- postordre brud nettsteder reddit

- postordre brud pГҐ ordentlig?

- postordre brud til salgs

- postordre brud tjenester

- postordre brud verdt det

- postordre brud wiki

- postordre brudbyrГҐ

- postordre bruddatingsider

- postordre brudebyrГҐer

- postordre brudefakta

- postordre brudekatalog

- postordre brudinfo

- postordre brudinformasjon

- postordre brudland

- postordre brudtjeneste

- postordre en brud

- postordre kone

- postordre koner

- postordre-brud

- potency

- Pouvez-vous commander un mail d'une mariГ©e

- PoЕЎta po narudЕѕbi mladenke

- poЕЎta za naruДЌivanje mladenke

- Prava narudЕѕba poЕЎte

- Prava narudЕѕba za mladenku

- Prave narudЕѕbe za mladenke

- precio promedio para la novia del pedido por correo

- primexbt-ltd.com

- prix moyen pour une mariГ©e par correspondance

- Prix ​​moyen de la mariée par correspondance

- Prix ​​moyen pour la mariée par correspondance

- Prix ​​moyens des mariées par correspondance

- PriДЌa za mladenku

- ProsjeДЌna cijena narudЕѕbe poЕЎte

- ProsjeДЌna cijena za mladenku za narudЕѕbu poЕЎte

- ProsjeДЌne cijene mladenke

- PU_m

- puedes enviar por correo a una novia

- punov

- pГҐ jakt etter ekteskap

- Qu'est-ce qu'une mariГ©e par correspondance

- Qu'est-ce qu'une mariГ©e par correspondance?

- Qu'est-ce qu'une mariГ©e.

- Qu'est-ce que la mariГ©e par correspondance

- Qu'est-ce que la mariГ©e par correspondance?

- Qu'est-ce que les services de mariГ©e par correspondance

- qual ГЁ il miglior servizio di sposa per corrispondenza

- que es como la novia del pedido por correo

- que es una novia de pedidos por correo

- que es una novia por correo

- que novia de orden de correo

- Quel est le meilleur pays de mariГ©e par correspondance

- Quel est le meilleur site de mariГ©e par correspondance

- quelle est une mariГ©e par correspondance

- Quelle mariГ©e par correspondance

- Quels sont les meilleurs sites de mariГ©e par correspondance

- rbjan

- rbnov

- Real Mail bestellen Braut Site

- Real Mail bestellen Brautwebsite

- real mail order bride

- real mail order bride service

- real mail order bride site

- real mail order bride sites

- real mail order bride stories

- real mail order bride website

- real mail order bride websites

- recensioni del sito web della sposa per corrispondenza

- recensioni di siti web per corrispondenza

- Recenzije agencije za mladenku

- reddit per corrispondenza legittima

- revisiГіn de la novia por correo

- revisiГіn de sitios de novias por correo

- Revue des sites des mariГ©es par correspondance

- RRRRRR

- rybelsus

- sann historie om postordrebruden

- se

- Service de mariГ©e par correspondance

- Service de mariГ©e par correspondance la mieux notГ©e

- Service de mariГ©e par correspondance rГ©el

- Services de mariГ©e par correspondance

- Services de mariГ©e par correspondance lГ©gitime

- Services de mariГ©e par correspondance supГ©rieures

- servicio de novias de pedidos por correo legГtimo

- servicio de novias por correo legГtimo

- servicios de novias de orden de correo superior

- servizio di sposa per corrispondenza legittimo

- should i buy a mail order bride

- should i date a mail order bride

- Site de la mariГ©e par correspondance des dix premiers

- site de mariГ©e par correspondance lГ©gitime

- Site de mariГ©e par correspondance rГ©el

- site de rencontres par courrier Г©lectronique

- site Web de la mariГ©e par correspondance

- site Web de mariГ©e par correspondance lГ©gitime

- sites de mariГ©e par correspondance

- sites de mariГ©e par correspondance les mieux notГ©s

- sites de mariГ©e par correspondance reddit

- sites de mariГ©e par courrier lГ©gitime

- sites de mariГ©e par courrier par correspondance

- Sites de mariГ©e Г commande par correspondance les mieux notГ©s

- sites de mariГ©es par correspondance

- sites de mariГ©s par correspondance rГ©els

- sites de rencontres par courrier Г©lectronique

- sites lГ©gitimes de mariГ©e par correspondance

- Sites Web de la mariГ©e par correspondance

- sites Web de la meilleure vente par correspondance

- Sites Web de mariГ©e par correspondance lГ©gitime

- Sites Web de mariГ©e par correspondance Reddit

- Sites Web de mariГ©es par correspondance

- siti di incontri per sposa per corrispondenza

- siti web per corrispondenza

- sitio de citas de novias por correo

- sitio web de la novia de pedidos por correo

- sitio web legГtimo de la novia por correo

- sitios de novias de orden de correo superior

- sitios de novias de pedidos por correo legГtimo

- sitios de novias de pedidos por correo real

- sitios legГtimos de novias por correo

- sitios web de novias de pedidos por correo real

- sitios web de novias por correo

- sito della sposa per corrispondenza legittimo

- sito della sposa per corrispondenza reale

- sito della sposa per corrispondenza superiore

- sito reale sposa per corrispondenza

- skal jeg gГҐ ut med en postordrebrud

- skulle jeg kjГёpe en postordrebrud

- slot-gacor-hari-ini

- slots

- So bestellen Sie eine Mail -Bestellung Braut

- So bestellen Sie eine russische Mail -Bestellung Braut

- So bestellen Sie Versandbestellbraut

- So datieren Sie eine Versandbestellbraut

- So erstellen Sie eine Versandbestellung Braut Reddit

- So machen Sie eine Mail -Bestellung Braut

- So maile die Braut beenden Bestellung

- Sober living

- SociГ©tГ©s de mariГ©e par correspondance lГ©gitime

- Software development

- Soll ich eine Versandungsbraut kaufen

- Sollte ich mit einer Versandbestellbraut verabreden

- Spinbit

- sposa interrazziale per corrispondenza

- sposa lesbica per corrispondenza

- sposa mondo per corrispondenza spose

- sposa per corrispondenza

- sposa per corrispondenza legittima

- sposa per corrispondenza per davvero

- sposa per corrispondenza piГ№ calda

- storie di sposa per corrispondenza

- storie di sposa per corrispondenza vera

- Suchen Sie eine Mail -Bestellung Braut

- Suchen Sie eine Versandbestellbraut

- Sumatriptan

- suosituimmat postimyynti morsiamen verkkosivustot

- sv+brittiska-kvinnor bästa rykte postorder brud

- sv+dating-com-recension bästa rykte postorder brud

- sv+guam-kvinnor bästa rykte postorder brud

- sv+heta-afrikanska-kvinnor bästa rykte postorder brud

- sv+heta-armeniska-kvinnor bästa rykte postorder brud

- sv+heta-karibiska-kvinnor bästa rykte postorder brud

- sv+jordanska-kvinnor bästa rykte postorder brud

- sv+libanesiska-brudar bästa rykte postorder brud

- sv+osteuropeiska-kvinnor bästa rykte postorder brud

- sv+spanska-brudar bästa rykte postorder brud

- sv+venezuelanska-kvinnor bästa rykte postorder brud

- SД±rada Posta Gelin

- Tarih Posta SipariЕџi Gelin

- Tech

- test

- test content

- th-best-slots

- th-casinos

- th-new-casinos

- th-new-slots

- the mail order bride

- the mail order bride site

- today-news

- todellinen postimyynti morsiamen verkkosivusto

- Top -bewertete Versandauftragsbrautseiten

- Top -bewertete Versandauftragsbrautservice

- Top -Mail -Bestellung Braut

- Top -Mail -Bestellung Braut Site

- Top -Mail -Bestellung Braut sitzt

- Top -Mail -Bestellung Brautdienste

- Top -Mail -Bestellung Brautlender

- Top -Mail -Bestellung Brautseiten.

- Top -Mail -Bestellung Brautwebsites

- Top 10 de la mariГ©e par correspondance

- Top 10 des sites de mariГ©es par correspondance

- Top 10 Mail -Bestellung Braut

- Top 10 Mail bestellen Brautwebsites

- top 10 mail order bride

- top 10 mail order bride sites

- top 10 mail order bride websites

- top 10 orden de correo novia

- Top 10 sites Web de mariГ©es par correspondance

- top 10 sposa per corrispondenza

- top 5 mail order bride sites

- Top 5 sites de mariГ©e par correspondance

- Top Bride Mail.

- Top deset narudЕѕbe za mladenku

- Top dix marins de la vente par correspondance webite

- Top Mail Bride Commande Web

- top mail bride order web

- top mail brudbeställningswebb

- Top Mail Command Bride Site

- top mail order bride

- top mail order bride countries

- Top Mail Order Bride se trouve

- top mail order bride services

- top mail order bride site

- top mail order bride sites

- top mail order bride sites.

- top mail order bride sits

- top mail order bride websites

- top mail sposi ordina web

- Top News

- top rated mail order bride service

- top rated mail order bride sites

- Top Ten Mail bestellen Braut

- Top Ten Mail bestellen Braut Site

- top ten mail order bride site

- top ten mail order bride webites

- top ten per corrispondenza sito sposa

- top ten per corrispondenza sposa webite

- top-news

- TOPNEWS

- topp 10 postorder brud

- topp 10 postordre brud

- topp 10 postordre brud nettsteder

- topp ordre brud

- topp ordre brud nettsted

- topp ordre brud nettsteder

- topp ordre brudland

- topp post brudebestillingsnett

- topp postorder brud

- topp postorder brud sitter

- topp postordre brud nettsteder.

- topp postordre brud sitter

- topp ti postordre brud nettsteder

- topprangerte postordrebrudesider

- tr-news

- Travail des mariГ©es par correspondance?

- trouver une mariГ©e

- Trouver une mariГ©e par correspondance

- Trouvez-moi une mariГ©e par correspondance

- trovare una sposa per corrispondenza

- True Mail -Bestellung Braut

- true mail order bride

- true mail order bride stories

- true story of mail order bride

- turkey

- turkey_cont_post_2

- turkey_cont_post_4

- una novia legГtima por correo

- una novia por correo

- una sposa per corrispondenza

- Uncategorized

- Une mariГ©e par correspondance lГ©gitime

- utenlandske bruder

- vad är den bästa postorderbrudwebbplatsen

- vad är en postorderbrud

- vad är postorderbruden?

- vale la pena la novia por correo

- vale la pena per la sposa per corrispondenza

- var hittar jag en postorderbrud

- vavada-slovenija.com

- vendita per corrispondenza siti sposa

- vendita per corrispondenza siti sposa legittimi

- vendita per corrispondenza sposa storie vere

- verdadera orden de correo novia

- veri e propri siti di sposa per corrispondenza

- verklig postorder brudens webbplats

- verklig postorder brudtjänst

- vero servizio di sposa per corrispondenza

- Versandbestellbraut definitiom

- Versandbestellbraut finden

- Versandbestellbraut wert?

- Versandbestellung Frau

- Versandbraut durchsuchen

- voitko tilata morsiamen postitse

- Wahre Geschichte der Versandbestellung Braut

- wahre Mail -Bestellung Brautgeschichten

- Was fГјr eine Mail -Bestellung Braut

- Was ist als Mail -Bestellung Braut

- Was ist der beste Versandauftragsbrautdienst?

- Was ist die beste Mail -Bestellung Braut.

- Was ist die beste Versandungsbestellung Brautland

- Was ist die Versandbraut?

- Was ist eine Mail -Bestellung Braut

- Was ist eine Mail -Bestellung Braut?

- Was ist eine Mail-Order-Braut

- Was ist Versandbestellbraut

- Was sind die besten Mail -Bestellbraut -Sites

- Was sind Postanweisungen Brautdienste

- Web mjesto za izlaske na narudЕѕbu poЕЎte

- Web stranica za mladenku

- Web stranice mladenke s najviЕЎe poЕЎte

- Web stranice za mladenke

- Web za narudЕѕbu s najviЕЎe poЕЎte

- what a mail order bride

- what are the best mail order bride sites

- what is a mail order bride

- what is a mail order bride?

- what is a mail-order bride

- what is as mail order bride

- what is mail order bride

- what is mail order bride services

- what is mail order bride?

- what is mail-order bride

- what is the best mail order bride service

- what is the best mail order bride site

- what is the mail order bride?

- what's a mail order bride

- whats a mail order bride

- whats a mail order bride?

- where can i find a mail order bride

- where can i get a mail order bride

- where do i buy a mail order bride

- where do i find a mail order bride

- where to buy a mail order bride

- where to find a mail order bride

- Wie funktionieren Versandbestellbraut -Sites?

- Wie funktioniert die Mail -Bestellung Braut?

- Wie funktioniert die Versandbraut, Braut zu bestellen?

- Wie funktioniert die Versandbraut, die Braut funktioniert?

- Wie funktioniert eine Versandbestellung Braut

- wie man beauftragte Braut

- wie man eine Braut bestellt

- Wiki de la mariГ©e par correspondance

- wikipedia correo orden novia

- Wikipedia Mail -Bestellung Braut

- Wikipedia Mail narudЕѕba mladenka

- wikipedia mail order bride

- wikipedia postimyynti morsian

- wikipedia postorder brud

- wikipedia postordrebrud

- Wo finde ich eine Mail -Bestellung Braut

- Wo kann man eine Versandbestellbraut finden

- Wo kann man eine Versandbestellbraut kaufen

- World

- World News

- world-news

- worldnews

- write an essay for me

- write essay for me online

- write my essay for cheap

- write my essay quick

- write my essay usa

- www.sigarenfabrieken.nl

- www.un-film-sur-riquet.fr

- www.weisse-magie.co

- xarelto

- xbetdownload.in

- yasal posta sipariЕџi gelini

- yasal posta sipariЕџi gelini sitesi

- ylimmän postin tilaus morsiamen sivusto

- zerkalo-pocket.ru

- Без категории

- ВїCuГЎl es el mejor servicio de novias por correo

- ВїCuГЎl es la novia del pedido por correo?

- ВїCuГЎles son los mejores sitios para novias por correo

- ВїCГіmo funciona la novia por correo

- ВїCГіmo funcionan los sitios de novias por correo

- ВїDГіnde puedo encontrar una novia por correo

- ВїPuedo obtener una novia por correo si ya estoy casado?

- ВїQuГ© es una novia de pedidos por correo?

- Г la recherche d'un mariage

- Г‚ge moyen de la mariГ©e par correspondance

- Г©pouses par correspondance

- ГЁ sicuro per corrispondenza sposa

- Гњst Nominal Posta SipariЕџi Gelin Hizmeti

- Гњst Posta SipariЕџi Gelin

- Гњst posta sipariЕџi gelin siteleri

- Д°yi posta sipariЕџi gelini web sitesi

- Д±rklararasД± posta sipariЕџi gelini

- ДЊlanci za mladenku

- Е to je mladenka kao narudЕѕba poЕЎte

- Е to je mladenka za narudЕѕbu poЕЎte?

- Е to je narudЕѕba poЕЎte

- Ећimdiye kadarki en iyi posta sipariЕџi gelini

- Новости Криптовалют

- Финтех

- Форекс Брокеры

- Форекс Обучение